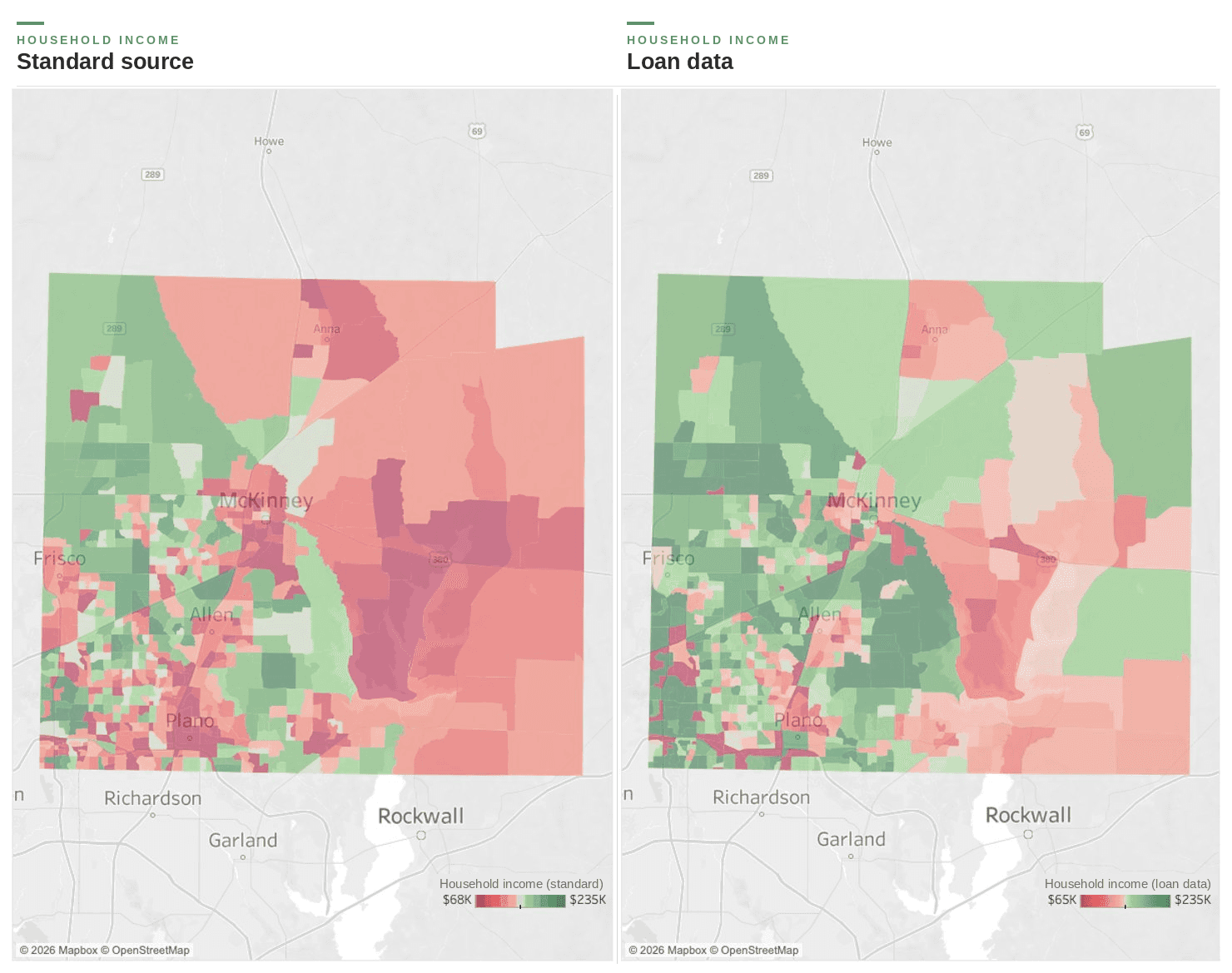

If you're pricing homes off Census or ACS income data, you're underestimating your buyer—and leaving money on the table.

Locate Alpha taps a unique loan data source that lets us see actual borrower incomes—not a survey average of everyone in a neighborhood, but what the people closing on homes really earn. We put it to the test: 12,300 loans originated in Collin County, Texas in 2025, with real approved-buyer incomes measured against the traditional sources builders lean on: Census, ACS, and the enhanced versions sold by data vendors. The gap isn't a rounding error. It's a different market—and it changes the math on what can be built where.

A 17-18% income gap

Traditional sources peg the median household income at $126,800. The loan data tells a different story: $165,500. That's a difference of $38,700, or roughly 17-18%.

The reason is simple. Census and ACS sample everyone in an area—renters, retirees, the unemployed, households with no intention of buying. The loan data behind Locate Alpha captures only the people who actually got approved to buy a home. When you're deciding what to build and how to price it, which group do you want to plan around?

What that gap buys

This isn't an academic distinction. Run that extra income through a standard 30% income-to-price ratio and it translates into about $130,000 of additional homebuying power per household.

For a builder, that flows straight to the land. It means roughly $26,000 more you can afford to pay on the lot—and a deal that pencils where it didn't before. The parcel you passed on last quarter because the numbers were tight might look very different when you're underwriting to the buyer who's actually showing up, not the statistical average of everyone in the ZIP.

Whole markets get re-rated

Zoom out and the picture changes at the area level, not just the household.

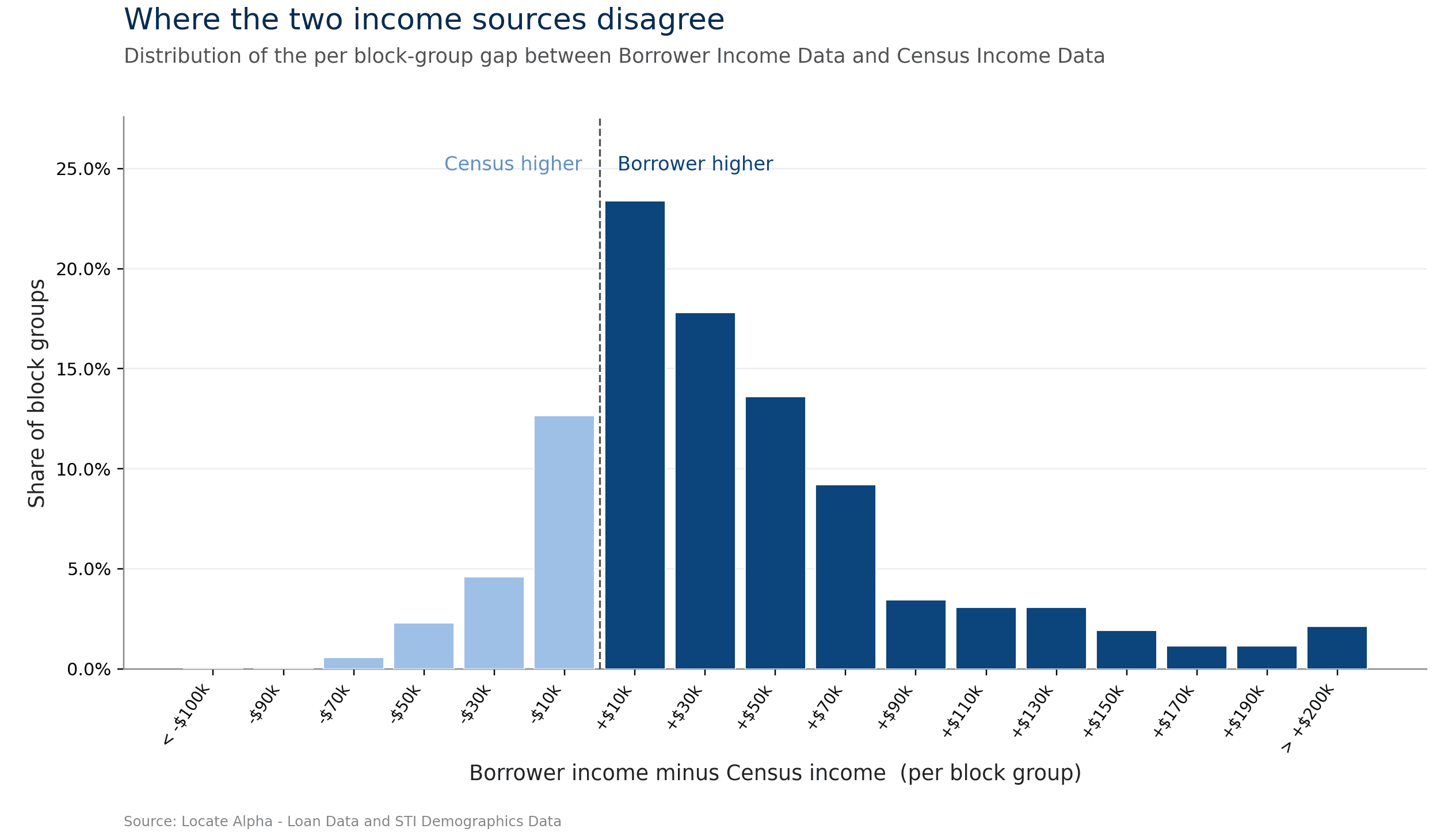

Across the block groups we analyzed, 84% had higher real incomes than traditional sources reported. In one in our block groups, true household income ran 33%+ above the published figure. These aren't outliers—they're the rule.

The distortion gets worse at the top. Traditional data effectively caps household income in the low $200Ks and captures nothing above it. Under that lens, only 10% of households look like $200K+ earners. Run the loan data and 28% clear $200K. That's nearly triple the high-income buyers that the conventional sources will ever let you see—buyers for move-up product, premium lots, and upgraded finishes you might otherwise assume the market can't support.

The takeaway

Traditional income data was built to describe a population. It was never built to describe your buyer. For homebuilders, that difference decides which deals close, which lots you win, and which product the market will actually absorb. By seeing real borrower incomes, Locate Alpha changes the math on what can be built where.

The demand is there. It's just hiding behind an average. Underwrite to the buyer who's qualified to purchase, and the map of where you can build profitably gets a lot bigger.